About GST Registration

Introducing Goods and Services Tax (GST) has been a big tax reform in India. And so much time has passed since its introduction that questions like “what is GST Registration” do not sound right. So here is a brief introduction

- GST is the only tax that one has to get his/her business registered under.

- If your business is not GST registered, heavy fines and penalties can be levied.

- GST Registration allows you to collect GST from your customers.

- So avoid going against the law, get your business registered for GST.

You can get your GST Registration through Maheswari Consultancy. Here, we excel in to lessen the burden of a lengthy registration process. Our expert team will guide you on how you can get GSTIN in a hassle-free way. You can apply anytime for your GST number whether you are based in Delhi NCR, Mumbai, Bengaluru, Chennai, or anywhere in India.

| Features | Central GST – CGST | State GST – SGST | Integrated GST – IGST |

|---|---|---|---|

| Tax Levied By | Central Government on Intra-State supplies of Goods and/or Services | State Government, on Intra-State supplies | Central Government, on Inter-State supplies |

| Applicability | Supplies inside a state | Supplies inside a state | Interstate supplies and import |

| Input Tax Credit | Against CGST and IGST | Against SGST and IGST | Against CGST, SGST, and IGST |

| Tax Revenue Sharing | Central Government | State Government | Shared between State and Central governments |

| Free Supplies | Applicable | Applicable | Applicable |

- Previous Law Converted Taxpayer – All individuals or companies registered under the Pre-GST tax laws like Service Tax or Excise or VAT, etc.

- Turnover for Goods Provider – If your sales or turnover of goods is crossing Rs. 40 lakh in a year then GST Registration is mandatory. For the Special Category Status, the limit is Rs. 20 lakh in a year.

- Turnover for Service Provider – If you are a service provider & sales or turnover is crossing Rs. 20 lakh in a year then GST Registration is mandatory. For the Special Category Status, the limit is Rs. 10 lakh in a year

- Casual Taxpayer – If you supply goods or services, in events/exhibitions, and not have a permanent place of doing business. In such cases, GST is charged based on an estimated turnover of 90 days. The validity of the Registration is also 90 days.

- Agents of Suppliers or Input Service Distributor (ISD) – All supplier agents and ISD, to earn benefits of Input Tax Credit, need GST Registration.

- NRI Taxable Person – If you are an NRI or handling the business of NRI in India.

- Reverse Charge Mechanism (RCM) – Businesses who need to pay taxes under the RCM also need to be GST registered.

- E-Commerce Portals & Sellers – Every e-commerce portal (such as Amazon or Flipkart) under which multiple vendors are selling their products. Or for all vendors. You need a GST Registration.

- Outside India Online Portal – For suppliers of online information and database access or retrieval services from a place outside India to Indian Residents.

- Transferee – When the business has been transferred.

- Inter-State Operations – Persons making an inter-state supply. Whatever the turnover.

- Brands – Aggregator who supplies service under his Brand or Trade Name.

- Other Taxation – Persons who are required to deduct tax u/s 37 (TDS) of the Income Tax Act.

- Voluntary GST Registration – Any entity can obtain GST registration at any-time. Even when the above mandatory conditions don’t apply to them.

- Inter-State Registration – If you are a supplier in more than one state you need GST Registration in all the states that you supply goods or services to.

- Branches – If your business has multiple branches in multiple states, register one particular branch as the main office or head office and the remaining branches as additional. (Not applicable if the business has separate verticals as listed in Section 2 (18) of the CGST Act, 2017.)

- Go to the Government GST Portal and look for Registration Tab.

- Fill PAN No., Mobile No., E-mail ID and State in Part-A of Form GST REG-01 of GST Registration.

- You will receive a temporary reference number on your Mobile and via E-mail after OTP verification.

- You will then need to fill Part-B of Form GST REG-01. To be duly signed (by DSC or EVC) and upload the required documents specified according to the business type.

- An acknowledgment will be generated in Form GST REG-02.

- In case any information is pending from your side. It will be sought from you by intimating you in Form GST REG-03. for this, you may be required to visit the department and clarify or produce the documents within 7 working days in Form GST REG-04.

- The office may also reject your application if they find any errors. You will be informed about this in Form GST REG-05.

- Finally, a certificate of registration in Finally, a certificate of registration will be issued to you by the department after verification and approval in Form GST REG-06

GST Certificate with ARN and GSTIN Number

GST Certificate with ARN and GSTIN Number

GST HSN Codes with Rates

GST HSN Codes with Rates

GST Invoice Formats

GST Invoice Formats

GST Return Filing Software

GST Return Filing Software

For Sole Proprietorship / Individual

- Aadhaar card, PAN card, and a photograph of the sole proprietor

- Details of Bank account- Bank statement or a canceled cheque

- Office address proof:

- Own office – Copy of electricity bill/water bill/landline bill/ property tax receipt/a copy of municipal khata

- Rented office – Rent agreement and NOC (No objection certificate) from the owner.

For Partnership deed/LLP Agreement

- Aadhaar card, PAN card, Photograph of all partners

- Details of Bank such as a copy of canceled cheque or bank statement

- Proof of address of Principal place of business and additional place of business :

- Own office – Copy of electricity bill/water bill/landline bill/ a copy of municipal Khata/property tax receipt

- Rented office – Rent agreement and NOC (No objection certificate) from the owner.

- In case of LLP- Registration Certificate of the LLP, Copy of board resolution Appointment Proof of authorized signatory- letter of authorization

For Private limited/Public limited/One person company

- Company’s PAN card

- Certificate of Registration

- MOA (Memorandum of Association) /AOA (Articles of Association)

- Aadhar card, PAN card, a photograph of all Directors

- Details of Bank- bank statement or a canceled cheque

- Proof of Address of Principal place of business and additional place of business :-

- Own office – Copy of electricity bill/water bill/landline bill/ a copy of municipal Khata/property tax receipt

- Rented office – Rent agreement and NOC (No objection certificate) from the owner.

- Appointment Proof of authorized signatory- letter of authorization

For HUF

- A copy of PAN card of HUF

- Aadhar card of Karta

- Photograph

- Proof of Address of Principal place of business and additional place of business :

- Own office – Copy of electricity bill/water bill/landline bill/ a copy of municipal Khata/property tax receipt

- Rented office – Rent agreement and NOC (No objection certificate) from the owner.

- Details of Bank- bank statement or a copy of a canceled cheque

For Society or Trust or Club

- Pan Card of society/Club/Trust

- Certificate of Registration

- PAN Card and Photo of Promotor/ Partners

- Details of Bank- a copy of canceled cheque or bank statement

- Proof of Address of registered office :

- Own office – Copy of electricity bill/water bill/landline bill/ a copy of municipal Khata/property tax receipt

- Rented office – Rent agreement and NOC (No objection certificate) from the owner.

- Appointment Proof of authorized signatory- letter of authorization

- All GST Returns must be filed by the 20th of the following month. There are strict laws under the GST Act for non-compliance with the Rules & Regulations.

- Penalty for Not Getting GST Registration, when a business is coming under the purview. The penalty is 100% of the tax amount if the offender has not filed for GST registration and intends to purposefully avoid it. The amount is the tax as applicable. Or Rs. 10,000, whichever is higher.

- A penalty of 100% tax due or Rs. 10,000, whichever is higher, is also applicable to those who choose Composition Scheme despite not being eligible to it.

- Any offender not paying his due tax or making short payments (genuine errors) is liable to pay a penalty of 10% of the tax amount. This amount cannot be less than Rs 10,000.

- A person guilty of not providing the GST invoice is liable to be charged 100% tax due or Rs. 10,000. Whichever is higher.

- An offender will be charged a fine of Rs. 25,000 for incorrect invoicing.

- If a person has not filed for unpaid tax, there is a penalty of Rs. 50 per day. Rs. 20 per day if he was to file for NIL returns. And the maximum amount must not exceed Rs. 5,000.

- There is also a provision of the penalty by a jail term for tax offenders to commit fraud.

A person who is not liable, still files for GST application, can get registered. However, then, it becomes essential for him to file Returns, after getting a GST number. Else, he will have to pay a penalty, as applicable.

You can choose to register for GST voluntarily too.

Especially if you are wishing to claim Input Tax Credit. Even if you are not liable to be registered, you can be registered voluntarily. After registration, you will also have to comply with regulations as applicable to those required to be registered.

Benefits of registering voluntarily under GST

- Take Input Tax Credit,

- Operate interstate without restrictions,

- Have the option to register on e-commerce websites,

- Have a competitive advantage compared to other rival businesses,

- Fewer hassles and better compliance with government licensing agencies,

- Focus on Your Business Growth.

Inputs are all those goods that went into creating the finished products provided to the final consumer. Businesses are charged GST on goods/services that are used as inputs. The ITC mechanism allows GST registered businesses to receive refunds on the GST paid for purchasing all inputs. This helps prevent the cascading taxation effect, which was the primary reason behind the introduction of the GST.

For instance: GST payable on the supply of the final product of a manufacturer is Rs. 850 and the GST paid on inputs is Rs. 725. The manufacturer can claim the Rs. 725 as ITC. This brings the net tax payable at the time of supply to Rs. 125 only (Rs. 850 – Rs. 725).

Under the previous indirect tax regime of levy of Service Tax, VAT, and Excise – a lot of input tax credit was not properly utilized.

Who are eligible to claim Input Tax Credit?

ITC is available only to those entities who have registered under the GST Act. Only GST registered businesses can claim ITC on the tax paid for the purchase of any business relevant inputs.

Who cannot claim ITC?

Input Tax Credit can be claimed only for business purposes. It is not available for goods or services exclusively used for:

- Personal use,

- Exempt supplies,

- Supplies for which ITC is specifically not available.

Apart from the above, there are some other cases where ITC will be reversed. Such as Credit Note issued to ISD, Non-payment of invoices within 180 days, assets bought partly or wholly for exempted supplies or personal use, etc.

Conditions for claiming Input Tax Credit

- GST invoice showing details of tax paid is necessary,

- The goods on which GST has been paid have been received by the consumer,

- The applicant has filed the relevant tax returns,

- The supplier had paid the due tax to the government,

- The ITC applicant is registered under GST,

- If goods were received in installments, ITC can be claimed only after the final lot has been received.

ITC cannot be claimed if

- Composition tax registered entities paying GST on inputs,

- If depreciation has been claimed on the tax part of a capital good,

- On goods not used as inputs such as supplies for personal use,

- On goods on which ITC is not applicable under the GST Act (exempted goods).

Input tax credits can be used as

- CGST input tax credits are allowed to be used to pay CGST and IGST,

- SGST input tax credits are allowed to be used to pay SGST and IGST,

- IGST input tax credits are allowed to be used to pay CGST, SGST, and IGST.

Small businesses with an annual turnover of less than Rs. 1.5 crore (Rs. 75 Lakhs for the Special Category States) can opt for the Composition scheme.

- Composition dealers need to pay nominal tax rates based on the type of business. (a maximum of 2% for manufacturers, 5% for the restaurant service sector and 1% for other suppliers.)

- Composition dealers are required to file only a single quarterly return (instead of the monthly returns filed by normal taxpayers).

- They cannot issue tax invoices. That is, they cannot collect tax from customers and they are to pay the tax out of their own pocket.

- Entities that have opted for the Composition Scheme cannot claim any Input Tax Credit.

Who can opt for the Composition scheme?

- All SMEs looking for lower compliance and lower rates of taxes under GST.

- A GST taxpayer, whose turnover is below Rs 1.5 crore, can opt for the Composition Scheme. (In the case of Special Category States, the present limit is Rs 75 lakh.)

- The Aggregate Turnover of all businesses registered under the same PAN would be taken into consideration to calculate turnover.

- Shall pay tax at normal rates in case he is liable under the reverse charge mechanism.

- Dealers of intra-state supply of goods (or service of only the restaurant sector).

Which businesses are not eligible to apply for the Composition Scheme?

Composition scheme does not apply to:

- Service providers,

- Inter-state sellers,

- E-commerce sellers,

- Supplier of non-taxable goods,

- Manufacturer of Notified Goods,

- All the suppliers of services except those providing restaurant services (not serving alcohol),

- Suppliers of – ice cream, pan masala or tobacco (and its substitutes),

- Casual Taxable Person,

- Non-resident Taxable Person,

- Supplier of exempted goods or services.

How to apply for the Composition Scheme?

- In case of new registration, you can opt for the scheme at the time of GST Registration.

- If you are already registered you can file for it by submitting GST CMP-02 online.

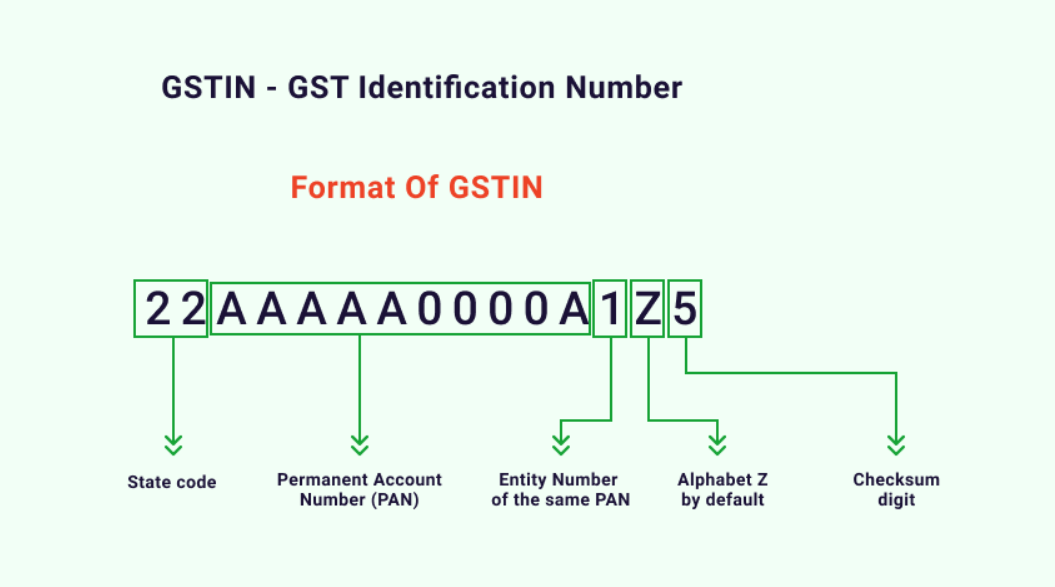

- GSTIN is a unique 15-digit alphanumeric code that is allotted to each Firm/Company/Individual, who are registered under GST.

- The government has ensured that everything under GST is digital so that there is maximum transparency with minimum corruption.

- The first 2 digits of the GSTIN represent the state code which is given as per the 2011 census.

- The next 10 digits are the PAN number of the entity.

- The 14th digit is Z by default.

- The 15th or the last digit is the Checksum digit. It comes, automatically, as a result of the calculation of the other 14 digits.

GST was rolled out nationwide on July 1, 2017.

It is a destination-based tax.

And follows a dual model in which both the State and the Central government levy tax on goods and services.

All businesses are required to obtain a GST number for every state that specific business has been registered in. The first step under the GST regime is to know whether the business is liable to register and register accordingly.

- You fill the application form given above.

- Mail the documents as required.

- Sit-back. All forms will be filed by us.

- Receive your GST number on e-mail.

Those providing services must get GST registration, once their turnover crosses Rs.20 lakhs and in case of Special Category States at Rs 10 lakhs.

- A supplier whose aggregate turnover is less than the prescribed limit and is not even covered under the mandatory GST requirement list.

- When supplies are covered under the Reverse Charge Mechanism (RCM).

- Those who are supplying non-taxable goods and services under GST.

- Agriculturists,

- Services by any Court or Tribunal established under the law,

- Services of crematorium, funeral, burial, mortuary, including transportation of the deceased,

- Sale of land/building subject to Schedule 5 (ii)(b). Actionable claims, other than betting, lottery, and gambling.

- Any specialized agency of UNO (United Nations Organisation) or any other multilateral financial institution and Organization notified under the United Nations Act, 1947,

- Consulate or Embassy of foreign countries,

- Any other person as notified by the Board/Commissioner,

- The Central Government or State Government may notify exemption from registration to specific persons

- They have to apply for registration at least 5 days prior to making any supply.

- Their registration certificate is valid for 90 days which can be extended.

- Registration is given or extended only when the person deposits the estimated tax liability.

- If you are involved in interstate supplies,

- You are a Casual taxable person or a Non-Resident taxable person,

- You are liable to pay tax under Reverse Charge Mechanism (RCM),

- You are supplying on behalf of a taxable person,

- Input service distributor (ISD),

- Selling on e-commerce platforms,

- You are an e-commerce operator,

- You supply online information and database access or retrieval services from outside India to an unregistered person in India,

- You are responsible for deducting TDS

- ease registration of GST online,

- computing and settling IGST,

- forwarding the taxes to Central and State authorities,

- matching tax payment items with the banking system,

- providing MIS reports to the Central and the State Governments based on the return information,

- running the network for reversal and reclaim of the input tax credit.

- Sales,

- Output GST (i.e. GST on sales),

- Input tax credit (GST paid on purchases).To file GST returns, only those sales and purchase invoices, that are GST compliant, are required. You can use our pocket-friendly GST Software to generate these GST compliant invoices.

- Voluntary Cancelation: When the tax-payer voluntarily cancels his or her GST registration.

- When he/she has reasons to believe that in the current financial year, the annual turnover will be less than Rs. 40/20 Lakh,

- The business operations have ceased to exist or have done amalgamation or any other arrangement.

- When the GST officer uses his power and cancels the certificate of the tax-payer. It may be because of the below reasons –

- If the tax-payer is not doing business from his/her notified registered place,

- If the tax-payer issues a tax invoice without making the supply of goods or services.

- You need to file Form Reg-16.

- Apply on the official GST website within 30 days.

- You will have to declare some important information in the application such as stock held on a particular date, amount of dues, credit reversal, and information about the payment made towards the discharge of liabilities.

- If the concerned officer is satisfied with the application and documents, the officer will cancel the same within 30 days.